The Equality of Price and Minimum Average Total Cost Yields

A competitive firm and market. If one unit costs a total of 20 then on average that one unit costs 20.

The Firm Under Competition And Monopoly

The equality of price and minimum average total cost yields technical _____ efficiency.

. The average total cost of one unit is 20. Occurs only in constant-cost industries. Results in a zero accounting profit.

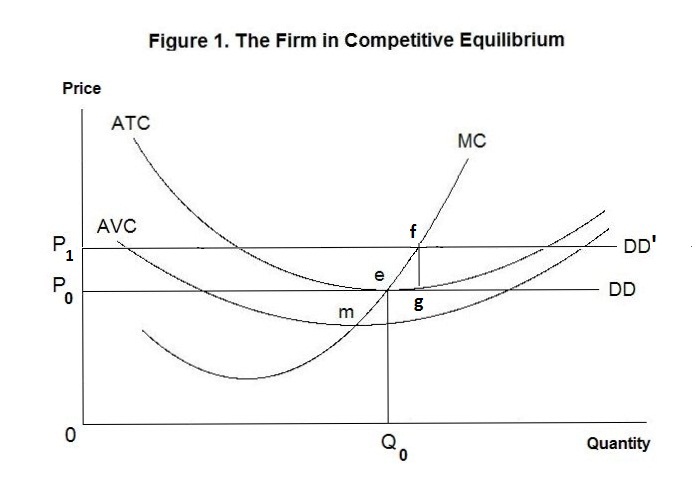

A The equality of price P marginal cost MC and minimum average total cost ATC at output Qf indicates that the firm is achieving productive efficiency and allocative efficiency. In the short run a firm that is a price taker would. Whereas the equality of price and MC yield allocative efficiency.

The most efficient technology B. In other words a factors price equals its marginal revenue product. Continue to produce a quantity such that marginal revenue equals marginal cost.

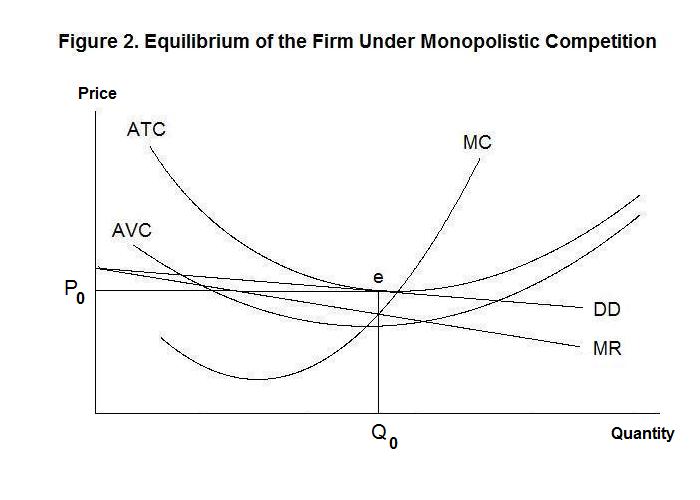

That is quantity on the horizontal axis multiplied by average cost on the vertical axis or 5 x 330 1650. Productive efficiency in monopolistically competitive markets does not occur in the long run because firms set the price. Price minimum average variable cost then firm stays in business.

Together they yield economic efficiency. Together they yield economic efficiency. The long-run equality of price and minimum average total cost means that competitive firms will use the most efficient know technology and charge the lowest price consistent with their production cost.

Means that the right goods are being produced in the right ways d. In long-run equilibrium the market price in a competitive price-taker industry will be equal to a. Encourages entry of new firms.

The equality of price and marginal cost yields _____ efficiency. Whereas the equality of PMC yield allocative efficiency. Under pure competition this outcome will be achieved as the long run equilibrium price of pure competitive firms would be at the min ATC.

D Price or marginal revenue will settle where it is equal to minimum average total cost. Now lets take a step back and find out something you might not have noticed first time around. C In the long run a multiple equality occurs where price equals marginal revenue which equals the minimum average total cost.

Monopolistically competitive firms do not achieve allocative efficiency because. As of now price equals both the marginal cost and the average total cost for each good P. On the demand curve where MRMC to maximize economic.

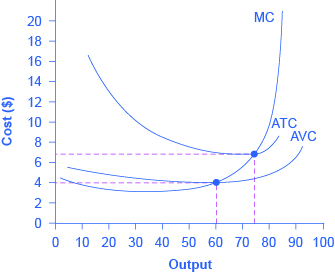

At this price and output level where the marginal cost curve is crossing the average cost curve the price received by the firm is exactly equal to its average cost of production. The fixed costs of production are 100. Average Total Cost Marginal Cost Market Price.

FIGURE 116 Long-run equilibrium. The equality of P MC and minimum ATC. Notice that the average variable cost plus the average fixed cost equals the average total cost.

Dbe brought back down to equality with maximum total cost in the long run. The equality of price and minimum average total cost yields _____ efficiency. The elasticities of the demand curves for firms in monopolistically competitive MC industries will become more like that of firms in pure competition as.

It is using the most efficient technology charging the lowest price and producing the greatest output consistent with its costs. Minimum average variable cost of production. The total variable costs are 64 for one unit 84 for two units 114 for three units 184 for four units and 270 for five units.

In Figure 96 the bottom part of the shaded box which is shaded more lightly shows total costs. The long-run market price equals the minimum average total cost ATC of producing the product. 3After all long run adjustments in a perfectly competitive industry product price will be exactly equal to and production will occur at each firms Amaximum average total cost.

That is the firm will achieve productive efficiency. The equality of price and marginal cost yields efficiency. Productive efficiency occurs where price is equal to minimum average total cost min ATC.

At this point firms must use the lease-cost technology or they wont survive. The equality of price and minimum ATC yields productive efficiency. And since suppliers will produce until marginal cost market price the long-run equilibrium in a purely competitive market can be summarized thus.

The equality of price and minimum average total cost yields efficiency. The long-run equality of price and minimum average total cost means that competitive firms will use the most efficient know technology and charge the lowest price consistent with their production cost. The equality of price and minimum ATC yields productive efficiency.

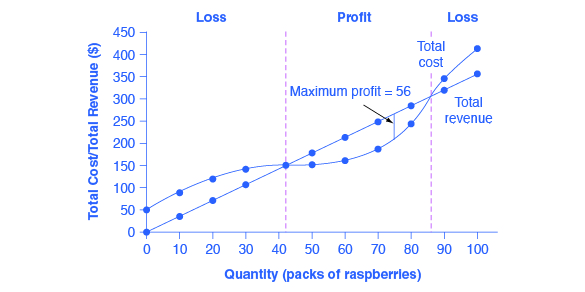

In long-run equilibrium the market price in a. The equality of the price and the minimum total average cost indicates that the company is using A. In the form of a table calculate total revenue marginal revenue total cost and marginal cost for.

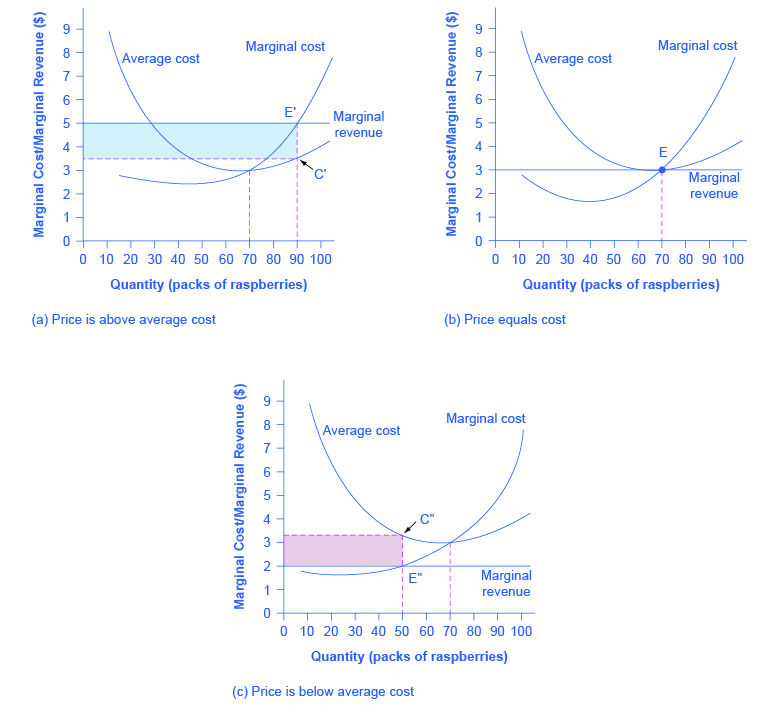

The farms total revenue at this price will be shown by the large rectangle from the origin over to a quantity of 70 packs the base up to point E the height. The sum of marginal and variable costs of production. Cminimum average total cost.

Minimum average total cost of production b. Minimum average fixed cost of production d. The equality of price and marginal cost yields _____ efficiency.

The equality of price and minimum average total cost yields technical _____ efficiency. When measuring industry concentration the four-firm concentration ratio is the percentage ratio of total industry _____ for the four largest firms in an industry. That is the firm will achieve productive efficiency.

Multiple models are used to study oligopolies because oligopolies. B In the long run a multiple equality occurs where price equals marginal cost which equals the minimum average total cost. Where P MC minimum ATC Reason.

The larger box of total revenues minus the smaller box of total costs will equal profits which the darkly shaded box shows. Any producer that maximizes profits faces a market price equal to its marginal cost P MC in perfect competition. A The equality of price P marginal cost MC and minimum average total cost.

The equality of price and marginal cost yields _____ efficiency. Suppose that price is below the minimum average total cost ATC but above the minimum average variable cost AVC and the market price is expected to rise at least to ATC in the near future.

8 2 How Perfectly Competitive Firms Make Output Decisions Principles Of Economics

Costs In The Short Run Principles Of Economics 2e

The Firm Under Competition And Monopoly

Reading Profits And Losses With The Average Cost Curve Microeconomics

Comments

Post a Comment